Welcome to Money Diaries where we are tackling the ever-present taboo that is money. We’re asking real people how they spend their hard-earned money during a seven-day period — and we’re tracking every last dollar.

Today: an editor who makes $80,000 per year and spends some of her money this week on health insurance copay.

If you’d like to submit your own Money Diary, you can do so via our online form. We pay $150 for each published diary. Apologies but we’re not able to reply to every email.

Occupation: Editor

Industry: Nonprofit

Age: 46

Location: Washington, D.C.

Salary: $80,000

Assets: I have $76,000 in my bank account (savings/checking) and $582,000 in me and my husband’s investment portfolio. The bulk of that, $492,000, is from stocks and mutual funds, and the remainder is two retirement accounts; one has $8,600 in it and the other has $81,000.

My husband, J., and I each have our own bank accounts. We also have a joint account that currently has $19,000 in it; we use that account to pay for utilities, groceries, clothes for our 11-year-old daughter, pet care, medical bills, vacations and anything else that falls under the general umbrella of family expenses. I’ve put $2,500 into that account each month since we opened it almost 20 years ago, and J. contributes $3,400 a month. Anything that J. and I buy for ourselves — clothes, personal items, meals out, gifts for each other or our relatives — comes out of our own accounts.

I came into our relationship with significantly more savings, which allowed us to put down 20% when we bought our house 12 years ago. J., who has always earned more money than me (his annual salary is $191,900), pays our monthly mortgage of $3,431 out of his personal account.

Debt: Remaining mortgage: $256,557; home renovation loan from my parents: $42,000.

Paycheck amount (2x/month): $2,331

Pronouns: She/her

Monthly Expenses

Mortgage: $3,431

Loan payments: $833 to my parents for the home renovation loan.

Gas: $22

Electricity: $90

Water: $130

Internet: $80

Netflix: $6.99

Hulu/Disney Plus/ESPN Plus Bundle: $15.89

Patreon: $5

Recurring donations: $50 to two different abortion funds.

Phone: I’m on our friends’ family plan (if anyone asks, we’re cousins) and they never ask for reimbursement.

House cleaner: $260 (twice a month).

Hebrew tutor: $180 (our daughter is studying for her bat mitzvah).

FSA: $400

401(k) contribution: $1,770

Health insurance: $742

Was there an expectation for you to attend higher education? Did you participate in any form of higher education? If yes, how did you pay for it?

There was definitely an expectation for me to attend higher education. My mother has a master’s and my father has an M.D. For both me and my older sister, the question wasn’t would we go to college but where. My parents also made it clear that they would contribute the same amount of money to my education as they did to my sister’s education. She went to a private college and I graduated from an in-state university so that meant that when I applied to graduate school, there was enough money left to cover that tuition. That said, my parents also encouraged me to apply for merit-based scholarships, one of which helped pay for my first semester of grad school.

Growing up, what kind of conversations did you have about money? Did your parent(s)/guardian(s) educate you about finances?

My parents didn’t really talk about money that much when my sister and I were in elementary school but at some point, when we were in our early teens, my mother began having discussions with us about our family’s finances. Her family had held stocks and other assets — land, real estate etc. — for generations; as a result, she knew a lot more about investing and the stock market than my father, who grew up in a more middle-class household. My mother taught us about dividend reinvestment, diversified portfolios, market volatility and other aspects of investing in stocks and mutual funds. But while my mother was open with us about our family’s finances, she and my father thought that talking openly about money wasn’t polite. My parents were also very frugal — they bought a new car once during my childhood and drove that for over 30 years; we didn’t take extravagant vacations or live in a huge house — and as a result, I thought that all my friends came from similar backgrounds. It wasn’t until I was in college that I realized that not everyone grows up with generational wealth. In retrospect, it’s embarrassing that it took me that long to figure it out.

What was your first job and why did you get it?

My first job that wasn’t babysitting or pet-sitting for neighbors was working in a small law office the summer before my senior year of high school. I got it because I wanted to earn my own money to buy clothes and CDs, and because at the time I wanted to be a lawyer.

Did you worry about money growing up?

I did, even though my parents never gave me a reason to worry about it. But I took books like A Little Princess and The Boxcar Children series way too seriously because I always had a fear that our family’s finances could change — for example, what if my dad lost his job? It wasn’t until I was in high school and my mother began to explain more about our finances that I stopped worrying so much.

Do you worry about money now?

Yes. I have chronic health issues that require a lot of surgeries, medications and doctors’ appointments to manage, and that’s made it difficult to consistently work full time. I spent a long time working as a freelancer because that made more sense with my health, but it also meant that I never had paid time off or sick leave, a 401(k), anything like that. And just taking care of myself is expensive. We have good health insurance through my husband’s job but because of how complex my issues are, there’s a lot that isn’t covered: treatments that are considered experimental, specialists that aren’t just out of network but out of the area. Because of the example my parents set, I’d probably live below my means even if I was healthy but knowing that, after our mortgage, my health is our largest yearly expense is a big reason that I worry about money. Based on the averages from the past six years, we spend $12,600 a year on out-of-pocket medical expenses, $3,200 a year on the tax-deductible health savings account, and $9,650 a year on health insurance.

At what age did you become financially responsible for yourself and do you have a financial safety net?

I started paying my own rent, utilities etc. after I graduated from college. But because of my health my parents paid to keep me on their health insurance until I went to graduate school two years later and qualified for coverage through my school. After I graduated, they insisted on putting me back on their insurance until I had a full-time job with benefits. So I’d say that I wasn’t fully financially responsible for myself until I was 27. My parents did pay for my wedding; they asked me and J. to keep the expenses under $10,000, which we were happy to do. My parents still help me and J. out financially but now it’s for our daughter, M. (their only grandchild). They’ve been putting money in her 529 account for years, and that’s a big reason that the account currently has over $130,000 in it. She goes to sleepaway camp each summer and my parents insist on paying for that. They also cover our travel expenses whenever we visit them or do any kind of travel that involves my family (for instance, if we meet in my sister’s city for the holidays, my parents pay for our hotel room). Thanks to their generosity and my mother’s financial acumen, I have a very strong safety net. I know how fortunate this makes me and I don’t take it for granted.

Do you or have you ever received passive or inherited income? If yes, please explain.

When each of my grandparents passed away, I received shares of stocks they had owned. And after I finished grad school my parents gave me a lump sum of $12,000, which I used to pay for rent, utilities and groceries until I found a job.

Day One

5:30 a.m. — Woken up by a severe muscle spasm in my right shoulder. I spontaneously developed spasms in my shoulders and neck about 15 years ago. They’re chronic so I’m used to the pain, but it’s still not fun. I get up and go to my favorite indoor pool for a half-mile swim. I swim three times a week, both because I like it and because exercise helps keep the pain manageable. (In addition to the spasms, I have chronic pain in my right wrist, which came out of nowhere when I was in college.) All city pools are free for D.C. residents, which is awesome.

8 a.m. — J. walks our two dogs while I go to my home office and check emails as I eat breakfast: Greek yogurt mixed with blueberries and granola. J. goes to work and M. pops her head into my office to announce her plan to stay in pajamas for as long as possible and read all morning. I try not to be too jealous since that’s what I’d like to do, too.

2 p.m. — Work is quiet, which is typical for a summer Friday. M. is going to sleepaway camp in a couple of weeks and has made a list of things she needs to buy, so we head out to the suburbs for some shopping.

5 p.m. — We find almost everything on her list: new clothes at Old Navy ($33.91) and Gap ($10.59), new Jibbitz at Crocs ($26.45), a battery-operated fan and more clothes at Target ($22.45), because M. keeps getting taller and outgrowing everything she owns, and a stationery set at Barnes & Noble ($18.95). I also buy an Auntie Anne pretzel ($5.29) for M. and a Starbucks chai latte ($5.38) for myself. $123.02

6:30 p.m. — Back home I wrap up work and feed the dogs, then throw together a tofu and pepper stir-fry for dinner. I find cooking relaxing and since I’m a vegetarian who occasionally eats fish, the whole family eats vegetarian at home. J. and M. clean up after dinner and we walk the dogs.

10:30 p.m. — After M. and I watch an Indigo Girls documentary on Netflix, I get ready for bed — brush teeth, wash face, apply Glow Recipe nighttime moisturizer — and decide which pain pills to take tonight. I take two medications every night to help me sleep and tonight I add a muscle relaxer to the mix. I fall asleep almost immediately.

Daily Total: $123.02

Day Two

8 a.m. — I wake up still in pain. We have friends coming over this afternoon so I decide to make chocolate babka. I learned how to make it during the early days of the pandemic and it’s become a family favorite. M. helps me mix the dough, then eats breakfast as I clean up the kitchen and put the dough aside to rise. J. gets up and he and M. walk the dogs while I start a load of laundry, take a shower and put on a cute sundress. The best piece of advice my mother ever gave me was that looking nice when you feel crappy can lift your mood, and that’s been true for me more often than not. I have some Diet Coke; it might be psychosomatic but sometimes I think the caffeine helps ease the spasm pain.

9 a.m. — I have a quick breakfast of cereal, milk and a banana. Inspired by last night’s documentary, M. and I decide to see if the Indigo Girls will be coming to the D.C. area anytime soon and find out that they’ll be here next month. J. decides that he’s not enough of a fan to go so I find two tickets for me and M. The tickets are $106 each and the fees add another $84. $295.76

10 a.m. — Time to run errands! J.’s brother and his wife just bought a house so we go to a home goods store in our neighborhood to buy them a housewarming present and a card ($27.03). Then it’s on to the farmers’ market for corn, mint, parsley, blueberries, tomatoes, radishes, garlic and scallions ($32.35). After that is the library; today they’re having a book and music sale where everything is $2. I buy two books and J. buys a stack of CDs ($22). $81.38

12 p.m. — The dogs jump all over us when we get home. I take them into the backyard and J. and M. leave again to go to an escape room in the suburbs, where they also have lunch; J. pays for the food and activity out of his own account. I take care of the laundry, do more babka prep and have a lunch of sliced peaches, yogurt, granola and a ton of water since it’s so hot outside. The spasms have subsided a little, which is a relief.

8 p.m. — Our friends have come and gone, we had a thrown-together dinner of leftovers and walked the dogs. M. asks for TV time and we tell her she can have an hour. The spasms are still pretty bad so J. and I go to our room so he can massage my shoulders with the massage gun he bought me for Hanukkah a few years ago. The massage leads to sex, which is a great way to end the day.

10:30 p.m. — After my regular nighttime routine, I take several drops of my THC/CBD tincture for the pain. Then I read in bed for a while before falling asleep.

Daily Total: $377.14

Day Three

7 a.m. — Wake up and take stock of the spasm situation. The pain has both spread and faded; now my neck and the base of my skull hurt, but it’s not as sharp as the past two days. I make a note to call my pain specialist tomorrow and make an appointment, although I’m not sure what treatment options are left — we’ve already tried dozens of medications, injections and more invasive treatments. I get out of bed and do my morning routine.

11:30 a.m. — M. and I pick up one of her friends and go to the pool. J. stays home to garden and read the paper like a stereotypical dad from the 1980s.

6 p.m. — M.’s friend is staying for dinner. J. and I feed the animals and then start our own meal prep. He makes salsa, I cook rice and we have black bean and rice bowls for dinner, with salsa, cheese and peppers. The girls say the bowls taste just like Chipotle, which I consider high praise.

7:30 p.m. — We’re almost out of produce and other random items so I run to the grocery store. On the sidewalk outside the store I chat with S., an unhoused man who’s been staying there for the past few months, and ask if he wants me to pick him up anything. He asks for bread, peanut butter, jelly, a few bottles of Gatorade and water, which I get along with the food for my family: berries, limes, tofu, pasta, shredded cheese, bananas, peppers, ice cream that’s on sale, black beans and a chocolate cake. $86.74

9:45 p.m. — Nighttime routine, including more THC/CBD tincture; I’m hoping this will be enough to finally calm down this spasm. I read in bed for about 15 minutes before falling asleep.

Daily Total: $86.74

Day Four

6 a.m. — The spasm is gone! I’m so happy to be at my normal level of pain that I practically leap out of bed. I feed the animals, let the dogs into the backyard, then do the rest of my morning routine before I start work in my home office. Since my pain tends to increase throughout the day, the mornings are my most productive time, so I feel fortunate that my employer is cool with my work hours basically being 7 a.m. to 3 p.m. I eat a breakfast of blueberries, yogurt and granola while I catch up on emails and the news.

8:15 a.m. — M. has a dentist appointment so we take the Metro to the dentist’s office. D.C. has a program where all kids under 18 can use the Metro system for free and my fare is covered by my employer. At the dentist, M. has to get two baby teeth pulled. All but $50 of the cost is covered by our dental insurance. $50

10:30 a.m. — Once we get home M. settles on the couch with the TV remote and an ice pack, and I go back to my home office. On an average week I go into my employer’s actual office once or twice but there’s flexibility in that; last week I worked an extra day in-office so that I could spend this whole week working from home.

1:45 p.m. — I receive a bill for an emergency room visit a couple of months ago, when I had severe pain in my kidneys and lower back. After, according to the statement, over $8,000 worth of testing and evaluation, the doctors discharged me without a diagnosis. With our insurance we owe $656.25, which is a hell of a lot better than it could be but still a major expense. $656.25

6 p.m. — J.’s working late so I feed the animals and make M. some very soft pasta for dinner. After she eats, I drop her off at a friend’s house for a sleepover.

7:15 p.m. — J. and I walk the dogs and talk about the hospital bill. We know how fortunate we are that we can absorb unexpected expenses like this and still have enough disposable income to buy things like concert tickets. At the same time, never knowing exactly how much each ER visit will cost is a constant source of stress; depending on what tests are ordered and how many doctors are called in to consult, they can run us anywhere from around $200 to over $1,000.

10 p.m. — Nighttime routine, this time without any extra pain meds on top of my usual ones. I’m living on the edge! Fall asleep after reading for half an hour.

Daily Total: $706.25

Day Five

5:50 a.m. — Wake up and go to the pool. Once I get home I feed the animals, put the dogs in the backyard, shower and then do the rest of my regular morning routine. I start work while eating a breakfast of yogurt, strawberries and granola. M.’s spending the day at her friend’s house so I have a very productive morning.

2:30 p.m. — One of J.’s closest friends has invited us to his daughter’s seventh birthday party this weekend. For her present, I order two books that M. loved at that age from our local bookstore. $12.70

6 p.m. — I pick M. up from her friend’s house. The girls are continuing the sleepover at our house so I chat with the other mom while M.’s friend gets her stuff together. J. gets home before us and feeds the animals, then I make teriyaki tofu for the first time while the girls set up M.’s room for the sleepover.

10 p.m. — Nighttime routine, read in bed for 20 minutes, pass out.

Daily Total: $12.70

Day Six

6:20 a.m. — I’m taking a few hours off this afternoon so I start work earlier than usual. Not too much came in after I logged off yesterday so I take advantage of the lull to prep my lunch, heating up leftover rice from last night with chopped garlic, sesame oil and olive oil, mixing in egg and pepper to make a dish that kind of resembles fried rice.

8 a.m. — J. and I walk the dogs after he eats breakfast. When we come home the girls are awake and ask if I can make eggs. After I do I notice that we’re running low on eggs and milk so I go to the grocery store to get those and the other food we’re running low on: cereal, strawberries, yogurt, granola, tortilla chips, ice cream, lemonade, bread and peanut butter. $79.46

12:10 p.m. — I wrap up work, the girls and I eat a quick lunch, and then we leave for the pool. After a lot of swearing and circling the block I finally find street parking near the pool ($4.60). It’s less crowded than the other day so although I usually don’t swim two days in a row, I take advantage of an empty lane and get my laps in. $4.60

3:30 p.m. — After the pool we drop M.’s friend off at her house and go home. I immediately jump on a call with my boss while M. studies Hebrew in preparation for her tutoring session tonight.

7 p.m. — After M.’s lesson, we have dinner: sautéed radishes, corn on the cob and fake meat. Dinner conversation revolves around M.’s bat mitzvah, which is about a year away. That sounds like a long time but there’s a lot she must do to get ready for it.

9:45 p.m. — Nighttime routine, then fall asleep almost as soon as I get into bed.

Daily Total: $84.06

Day Seven

7 a.m. — My happiness at sleeping in immediately evaporates when I realize that due to a water main break down the block, we have no water. J. talks with the repair guys and finds out that the break won’t be repaired until noon at the earliest. I feed the animals, then he and I walk the dogs. Once we’re home, we put all the ice cubes in our fridge into a pitcher so that there’ll be water for the animals and M.

8 a.m. — J. goes to the office and I start work, feeling a little bit guilty that the chaos of the morning has me logging in later than usual. I eat the same breakfast as yesterday because I am a boring creature of habit. M. sleeps late, too. After she wakes up and hears about the water situation, she decides to go to a friend’s house.

4 p.m. — The water’s back on! I celebrate by starting a load of laundry — I am perpetually surprised by how the three of us generate so much laundry each week — and then try to fix my ancient printer, which has apparently chosen today to finally die.

6:45 p.m. — M., J. and I decide to get takeout from our favorite Chinese place. When J. goes to pick up the order, he realizes that the food was accidentally charged to my dad’s credit card, which was stored as the default card on the restaurant’s ordering platform after my parents bought us dinner there during their last visit. I text my dad to warn him about the charge and tell him we’ll repay him; he replies that he’s happy to have bought us dinner, which is very sweet of him.

10:30 p.m. — I’m almost to the end of Cue the Sun! and really want to finish tonight but I’m too tired. It’ll have to wait until tomorrow.

Daily Total: $0

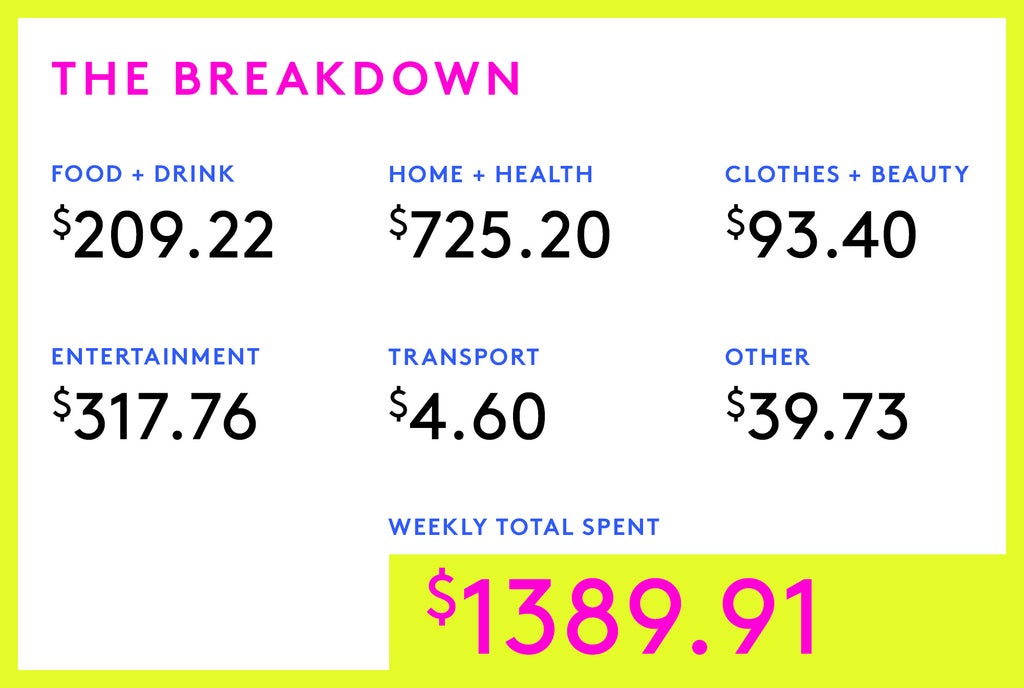

The Breakdown

Weekly Total $$ Spent: $1389.91

Food & Drink: $209.22

Entertainment: $317.76

Home & Health: $725.20

Clothes & Beauty $93.40

Transportation $4.60

Other $39.73

Money Diaries are meant to reflect an individual’s experience and do not necessarily reflect Refinery29’s point of view. Refinery29 in no way encourages illegal activity or harmful behavior.

The first step to getting your financial life in order is tracking what you spend — to try on your own, check out our guide to managing your money every day. For more Money Diaries, click here.

Do you have a Money Diary you’d like to share? Submit it with us here.

Have questions about how to submit or our publishing process? Read our Money Diaries FAQ doc here or email us here.

Like what you see? How about some more R29 goodness, right here?

A Week In Northern California On A $109,000 Salary

A Week In Pittsburgh, PA On An $80,000 Salary

A Week In New York On A $204,000 Salary

from Refinery29 https://ift.tt/TXK8EgH

via IFTTT